The Chicago SMART Tax

Pathways to Recouping Big Tech Tax Avoidance

The global economy is increasingly characterized by a digital enclosure movement, wherein the social interactions, data, and attention of billions are commodified by a handful of technology conglomerates — like Alphabet (Google), Amazon, Apple, Meta, Microsoft, Netflix, etc. While these mega-entities generate trillions of dollars in value, they have historically operated with a level of fiscal impunity that undermines the social contract of taxation and leaves government without adequate resources.

The passage and implementation of the Social Media Amusement and Responsibility Tax (SMART) in Chicago represents a pivotal shift in this dynamic — a first-of-its-kind mechanism designed to compel Big Tech to reinvest in the very communities from which it draws its wealth. The Institute for the Public Good, led by Ishan Daya and Julie Dworkin, built a proposal around the social media tax, which the City of Chicago Mayor's Office used to inform the current version of the SMART (amusement) tax. The tax revenue collected will be invested in funding the pillars of the Treatment Not Trauma campaign — continued re-opening and full funding of public mental health centers in Chicago and the expansion of the non-police crisis response for behavioral and social needs crises.

This progressive tax measure was adopted by a grassroots campaign — Babies Over Billionaires — led by the People's Unity Platform, which argued that the city's $1.2 billion budget deficit was the result of decades of fiscal mismanagement by mayors previous, corporate welfare, and a failure to enact progressive revenue options. This campaign demand was ultimately adopted and adapted by Mayor Johnson's administration as part of the "Protecting Chicago" budget proposal for 2026.

This report examines the economic dimensions of the SMART tax and explores this new revenue source in the broader struggle for economic equity, public health, and the expansion of the public good.

Updates · June 2026

Updates since this report was published

This report was originally published in March 2026. Several major developments have followed.

Illinois enacted a digital advertising tax

The FY27 state budget signed on June 16, 2026 includes a levy on digital advertising — one of the very measures this report tracked moving through statehouses. State budget leaders are not yet counting on its revenue, anticipating that it will be challenged in court, and Gov. Pritzker said he feels more confident the social media tax will hold up. (Chicago Sun-Times)

Illinois adopted the SMART tax structure at the state level

The same budget package establishes a state social media tax — one that social media companies pay based on the number of Illinois users they have, modeled on Chicago's approach — with the state banking on roughly $200 million from it. The per-user structure will now operate at both the city and state levels. (Chicago Sun-Times)

Chicago's collections are outpacing projections — amid ongoing litigation

The SMART tax was projected to raise $31 million in 2026. The city collected $16.4 million in the first four months alone, putting it on pace for about $49.2 million — roughly 59% above the original estimate. Meanwhile, the social media lobby is challenging the tax: the revenue is being held in escrow pending a First Amendment lawsuit filed in March by the tech-industry group NetChoice. (Chicago Sun-Times)

01 — The Political Economy

Digital Extraction and Corporate Tax Avoidance

For the better part of two decades, the "Silicon Six" — Alphabet, Amazon, Apple, Meta, Microsoft, and Netflix — have reshaped the domestic and global economy while successfully navigating a tax landscape that allows them to avoid hundreds of billions in federal and local obligations. This evasion is not merely a technical loophole but a core feature of a business model that prioritizes shareholder returns over the stability of the municipalities and public good systems that provide the infrastructure and human capital for their product and operations.

The Magnitude of the Global Tax Gap

Analysis of the financial performance of the top technology firms between 2015 and 2024, by the Fair Tax Foundation, reveals a staggering disparity between global profits and cash taxes paid. Collectively, these six companies generated over $11 trillion in revenue and $2.5 trillion in profits over the last decade. However, the effective corporate income tax rate they faced across the globe was only 18.8%, a figure that drops to 16.1% when excluding one-off repatriation payments. This occurs at a time when the average headline corporate income tax rate in the United States was 29.7% and the global average was 27.0%.

In those same years (2015–2024), Meta, Apple, Google, Microsoft, Amazon, and Netflix avoided a total of $144 billion in taxes paid to the federal government, ranging up to $299 billion if we were to remove the structural tax cuts afforded within the Tax Cuts & Jobs Act of 2017.

The mechanisms of this avoidance are rooted in the exploitation of intangible assets — such as patents, marketing rights, and algorithms — which are easily relocated to low-tax jurisdictions to shift profits away from high-tax areas where revenue is actually generated. In the United States, the Foreign-Derived Intangible Income (FDII) tax break has further insulated these companies, providing a $30 billion benefit over just three years and reducing effective tax rates by as much as five percentage points for companies like Meta and Alphabet. This systemic under-taxation fuels income disparity, as the wealth generated by the labor and data of the working class is concentrated in the hands of a few billionaires while the public treasury is starved of the funds needed for education, housing, and healthcare — systems that lift people out of poverty.

The Monetization of the Attention Economy

The business model of social media companies is fundamentally predicated on commandeering the eyes and attention of users — an anchor to this new attention economy. This model is measured by the Average Revenue Per User (ARPU). For a platform like Meta, the typical user in North America is worth approximately $26.73 per month in advertising revenue. On an annual basis, a single Meta user generates over $320 for the company — revenue that is largely derived from the data the user provides, the content they create, and the attention they sacrifice to the platform's algorithms.

The Psychological Externality: Mental Health as a Public Cost

The negative implications of social media usage on community wellbeing are well-documented and represent a massive, uncompensated externality. The Surgeon General has issued advisories concluding that social media presents a "meaningful risk of harm" for youth, citing addictive design patterns that contribute to rising rates of depression, anxiety, and mental illness.

Social media exposes youth to harmful content that can lead to dangerous and unhealthy behaviors. Examples include depictions of illegal activities, self-harm, and views of people's lives and bodies that are not realistic, which can lead to self-injuring, eating disorders, or even suicide in some cases. Studies also found that discussing or showing this content can normalize these behaviors.

A review of 50 studies across 17 countries between 2016 and 2021 published in PLOS Global Public Health suggested that relentless online exposure to largely unattainable physical ideals may trigger a distorted sense of self and eating disorders. Social media platforms also can expose teens to cyberbullying and sexual predators. These platforms utilize aggressive algorithmic strategies to maintain engagement, often at the expense of the psychological health of cities' most vulnerable residents.

The macroeconomic cost of this crisis is profound. Mental health issues are estimated to cost the U.S. economy approximately $282–477 billion annually in lost productivity and healthcare expenses — bringing Chicago's relative cost range to anywhere between $2.3–$3.8 billion. In cities across the country, the lack of accessible mental health resources often forces a reliance on law enforcement as a default crisis responder, which is both economically inefficient, socially destructive, and leads to worse health outcomes. By failing to internalize the costs of the mental health crisis they help fuel, social media companies are essentially subsidized by the public health and safety budgets of the city.

02 — The National Picture

The Landscape of Digital Taxation

The Chicago SMART tax is a marker in a long evolution in digital taxation policy. Across the country, state and local governments have recognized that their tax codes are designed for an industrial economy of physical goods and are failing to capture the value of a service-oriented digital marketplace.

The Maryland Digital Advertising Tax (DAT)

Maryland was a pioneer in this field, enacting the first-in-the-nation digital advertising tax in 2022. The tax applies to entities with at least $100 million in global ad revenue and $1 million in Maryland gross revenues. However, the law was immediately mired in litigation. The primary legal hurdle arose from a "pass-through" ban that prohibited companies from explicitly listing the tax on commercial invoices to ad buyers. In 2025, the U.S. Court of Appeals for the 4th Circuit ruled that this provision violated the First Amendment as an unconstitutional restriction on speech, though the tax itself remained in effect for those who could navigate the legal landscape.

Chicago's SMART tax differs from Maryland's by focusing on "amusement" rather than "advertising services." By framing social media as an entertainment service — an "amusement" in the legal sense — Chicago leverages its home-rule authority and established precedents for taxing digital goods like streaming media.

Comparative Efforts in Other Jurisdictions

Other states have followed suit with varying degrees of success. In New York, community organizations and advocates are pushing for a graduated data collection tax on for-profit entities that are mining consumer data.

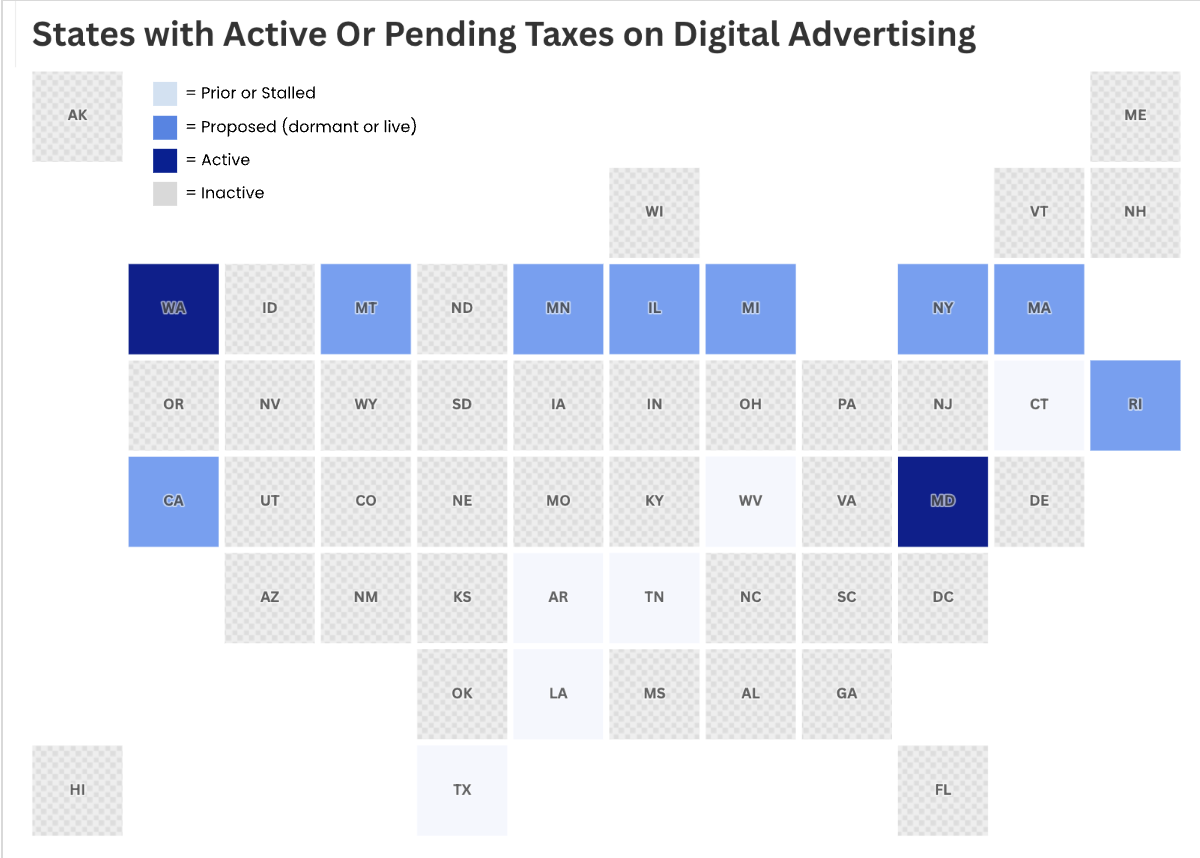

The Chicago SMART tax is the first ripple in a hopeful wave of social and fiscal accountability for social media companies and Big Tech that is sweeping the nation. It is also a part of a broader agenda that is working to modernize this city, state, and country's tax regime from the industrial tax policies we've held over to a modern, digital age. A key part of that fight is the movement to tax digital advertising revenue. In 2025 and 2026, this movement has grown beyond Maryland.

States with Enacted or Active Digital Advertising Taxes

- Maryland: The first and only state to fully implement a digital advertising gross revenues tax. It uses a graduated rate (2.5% to 10%) for companies with at least $100 million in global annual gross revenue. Revenue is earmarked for the state's education system.

- Washington: Effective October 1, 2025, Washington expanded its sales and use tax base to specifically include digital advertising.

States with Active or Proposed Legislation (2025–2026)

- California: Assembly Bill 796 (2025) and Assembly Bill 2829 (2023-2024 session) propose a tax on gross revenues from digital advertising for entities with at least $100 million in annual revenue. Net proceeds are intended to fund youth mental health services and social media protections for minors.

- New York: Senate Bill S4778 (Active for 2025-2026) aims to establish a tax on digital ads for persons with annual gross revenues in the state of $100 million or more.

- Rhode Island: Senate Bill S2028 (Introduced January 2026) proposes a sales tax on digital advertising services effective July 1, 2026. The rate varies from 2.5% to 7.5% based on global revenue thresholds. Net proceeds are intended to fund public transit, climate resiliency, housing development, the universal lunch program, and municipal resiliency plans, with a portion also going to the general fund.

- Massachusetts: Multiple measures are under consideration, including House Bill 3224 (6.25% rate) and House Bill 3089 (2025) specifically targets companies making more than $1 million annually from ads aimed at Massachusetts residents.

- Michigan: House Bill 4142 (Introduced February 2025) proposes the "Digital Advertising Services Tax Act." It features a graduated rate topping at 10% for companies with over $15 billion in global annual gross revenue.

- Illinois: While a 10% tax on digital advertising was considered for the FY 2026 budget, it was ultimately not included in the final measure passed in June 2025 due to industry opposition, but is being revived for FY 2027 as HB 4894 and SB 3353. Governor JB Pritzker has proposed a similar tax to raise $200M for FY26-27.

- Montana: Lawmakers have proposed legislation (Draft Bill 1649) that includes a 10% tax on digital advertising revenue for large global earners.

States with Prior or Stalled Proposals

While these states do not have active 2026 legislation moving through committees, they have formally debated or introduced measures since 2021 that established the current legislative framework:

- Arkansas: Debated Senate Bill 558 to add a user tax to social media platforms with 500,000+ account holders.

- Connecticut: Introduced several proposals starting in 2021; however, recent 2025-2026 budget priorities have focused on different tax credits and rebates rather than a new digital ad tax.

- Other Southern States: Lawmakers in Texas, Tennessee, Louisiana, and West Virginia have previously introduced similar measures, though most failed to pass out of committee.

03 — Chicago Leading the Charge

The Social Media Amusement and Responsibility Tax

The enactment of the SMART tax represents a watershed moment for municipal finance and social policy. By redefining the social media experience as a taxable amusement, the City of Chicago has established a clear legal and economic framework for holding Big Tech accountable to the public good.

The Mechanics of the SMART Tax

Codified in Municipal Code, the SMART tax applies to social media businesses that qualify as amusements, that collect consumer data from more than 100,000 Chicago consumers in a calendar year. The tax is structured as a per-user fee rather than a gross receipts tax, which simplifies administration and aligns it with the per-person nature of data collection.

per active Chicago consumer, per month.

each year — focusing the tax on large multinational platforms while exempting local start-ups and smaller community platforms.

Engagement with media content delivered through social media for the substantial purpose of entertainment and enjoyment — including images, video, audio, and artificial intelligence-generated content.

To establish if a user is outside of Chicago, businesses may use existing data (IP addresses, account registration) to identify Chicago consumers.

For a platform like Meta, which has millions of users in Chicago, the tax is calculated monthly. If a company has 1,500,000 active users in Chicago in a given month, they are taxed on 1,400,000 of them (after the exemption), resulting in a monthly liability of $700,000. With just the top eight social media companies operating in the city, the tax is projected to raise $31 million annually.

One of the most momentous aspects of the SMART tax is the establishment of the Protecting CARE Fund. This special revenue fund is dedicated exclusively to support for the city's mental and behavioral health operations and investments.

Historically, Chicago's most innovative mental health initiatives, such as the CARE (Crisis Response and Engagement) teams, were funded by temporary federal pandemic relief (ARPA) dollars. As these funds are set to expire at the end of 2026, the SMART tax provides a permanent, sustainable revenue stream that allows these programs to further move into the city's Corporate Fund and eventually the dedicated Protecting CARE Fund starting in 2027.

Interactive

Estimate a platform's liability

The SMART tax is calculated monthly, following the report's own worked example: a platform owes $0.50 per active Chicago consumer per month, with the first 100,000 users exempt. Move the slider to see what any given platform would owe.

SMART Tax liability calculator

Monthly liability = $0.50 × (active Chicago users − 100,000 exempt).

04 — Counterarguments & Rebuttals

Addressing the Opposition

The implementation of the SMART tax has faced fierce opposition from corporate interests. Addressing these arguments is essential for maintaining a broad coalition of support across the political spectrum.

Invasive Data Collection. The business community has expressed concerns that the tax will force companies to collect "sensitive location data" to verify who is a Chicago consumer, potentially violating user privacy.

Social media companies are already among the most invasive data collectors in history. They track user location, IP addresses, and behavioral data with extreme granularity to sell targeted advertising. The ordinance explicitly states that it does not require companies to collect any additional data beyond what they already use for their standard business purposes. These companies regularly report out on user counts by locality — this would be a shallower reporting requirement than what their current internal reporting requirements yield. The city is merely asking companies to aggregate the data they are already collecting to determine their tax liability. If these companies can accurately target a Chicagoan with an ad for a local restaurant, they can accurately count that user for the SMART tax.

Cost Passthrough To Consumers. Critics of the SMART tax claim that its costs will be passed down to consumers and small businesses.

However, the incidence of such taxes is more complex. In two-sided markets like social media, platforms must balance the number of users with the number of advertisers. If they raise fees too high for users or advertisers, they risk losing the network effects that make them profitable in the first place. Furthermore, for the individual user, the use of the platform is "free" and inherent to the business model of these social media companies. The SMART tax does not charge the user; it charges the platform.

Chicago Company Attrition. Will companies leave the city?

Social media platforms derive their value from "network effects" — a flywheel created that when there are more users, there's more content generated, and more value for both the platform and the potential ad buyers. This makes the Chicago user base a "location-specific" asset that these companies cannot easily replace. By taxing the access to this user base, the city is effectively extracting a portion of the "rent" these companies earn from Chicago residents. In essence, this tax structure makes it not matter whether or not a business is located in Chicago — and taxes only the assets within Chicago.

Doesn't Go Far Enough. An argument could exist that a $0.50 tax per user does not tax the full value a social media company is getting from selling personal data. A proposal like a digital advertising tax which essentially extracts value every time a person's data is used for financial benefit could generate more revenue and create more accountability.

Chicago has limited home rule authority when it comes to taxing income or earnings and needed to stay within a framework that had already been legally vetted — the amusement tax. Certainly, there is more that can be done at the state and federal level when it comes to taxing social media companies, but this proposal represented a creative local taxation solution that could be implemented immediately. Ultimately, in order for municipalities, states, and the federal government to be able to better craft tax measures that hold these companies accountable, our legal frameworks need to catch up to the digital age.

05 — Conclusion

A New Social Contract for the Digital City

The enactment of the Social Media Amusement and Responsibility Tax is a historic achievement for those working to hold Big Tech accountable across the nation. By linking the immense wealth generated from digital extraction to the growing need for mental health care and non-police crisis response, Chicago has created a model where cities can push large social media companies to mitigate the negative externalities associated with their products and practices, and re-invest in the cities and states in which they extract value.

These policies are gaining momentum across the country as more localities see successful interventions being used across municipalities and states that claw-back the taxes avoided federally, to go towards funding their Public Good.

Most recently, in February 2026, Governor Pritzker and the State of Illinois took inspiration from Chicago, and states like Minnesota, and proposed a similar tax in their FY27 budget — one that tells social media companies to pay a graduated rate per user in Illinois, generating $200M that is proposed to be used for education.

References

Sources

- Fair Tax Foundation, Silicon Six Report 2025. fairtaxmark.net

- Voronoi — "How much money do social media platforms make from you." voronoiapp.com

- U.S. Surgeon General, Youth Mental Health and Social Media Advisory. hhs.gov

- Yale Medicine — "Social Media and Teen Mental Health: A Parent's Guide." yalemedicine.org

- Yale News — Study quantifying the economic costs of mental illness in the U.S. news.yale.edu

- Meharry School of Global Health & Deloitte — analysis of mental health inequity costs. meharryglobal.org

- Illinois Answers Project — Chicago budget coverage. illinoisanswers.org

- Sales Tax Institute — "Expanding the Digital Tax Net." salestaxinstitute.com

- State and Local Tax — Fourth Circuit ruling on Maryland's digital ad tax pass-through prohibition. stateandlocaltax.com

- Avalara — "New York introduces data collection tax / digital ad tax again." avalara.com

- SEIU Healthcare Illinois — bold revenue legislation (HB 4894 / SB 3353). seiuhcilin.org

If you have additional questions on this report, or if you would like to discuss a similar policy for your locality (municipal, county, or state), please reach out to comms@i4pg.org.